2026 SECOND QUARTER COMMENTARY

LOCAL MARKETS IN A NUTSHELL

Over the quarter the FTSE/JSE All Share Total Return Index fell a modest -0.61%. Industrials were the hardest hit down -8.75% followed by financials at -2.01%. Resources has a great quarter with a gain of 7.23%. Surprisingly South African Mid and Small Cap stocks (a proxy for South African-centric stocks) were up 3.04% for the quarter.

South African bonds were down -2.9% for the quarter after having delivered 9% in the previous quarter.

Chart: Performance of the FTSE/JSE All Share Index over the past ten years.

Source: tradingeconomics.com

The quarter was off to a great start with the local equity market delivering an 11% return in the first two months. The local bond market returned 4% over the same period.

As a result of the US war with Iran, March delivered a sobering -10.5% from local equities, whilst local bonds fell -6.6%.

The war has unfortunately resulted in an increase in inflation expectations which could impact interest rates. It was believed that the South African Reserve Bank (SARB) would lower interest rates by 0.5% over the course of the year. Depending on the outcome of the war and inflation expectations, the SARB may delay interest rate cuts. There are also fears that if the situation in the Strait of Hormuz drags out, the SARB may need to hike interest rates, leading to a higher cost of capital which typically isn’t good for certain South African centric companies.

South African GDP for 2025 came in at 1.1% compared to National Treasury’s estimate of 1.4%. If one looks at national Treasury’s GDP forecasts against what actually transpired, they consistently overestimate South Africa’s GDP growth.

Although growth in South Africa is accelerating, it’s far from where we need it to be. A large driver of economic activity in South Africa is from household consumption. With the increase in the fuel price, inflation expectations increased materially. Should the SARB find itself in a position where it needs to increase interest rates to control inflation, household consumption could decline along with overall GDP.

Conversely, if there is a positive outcome in the Strait of Hormuz, the outlook for interest rates and inflation in South Africa could materially improve.

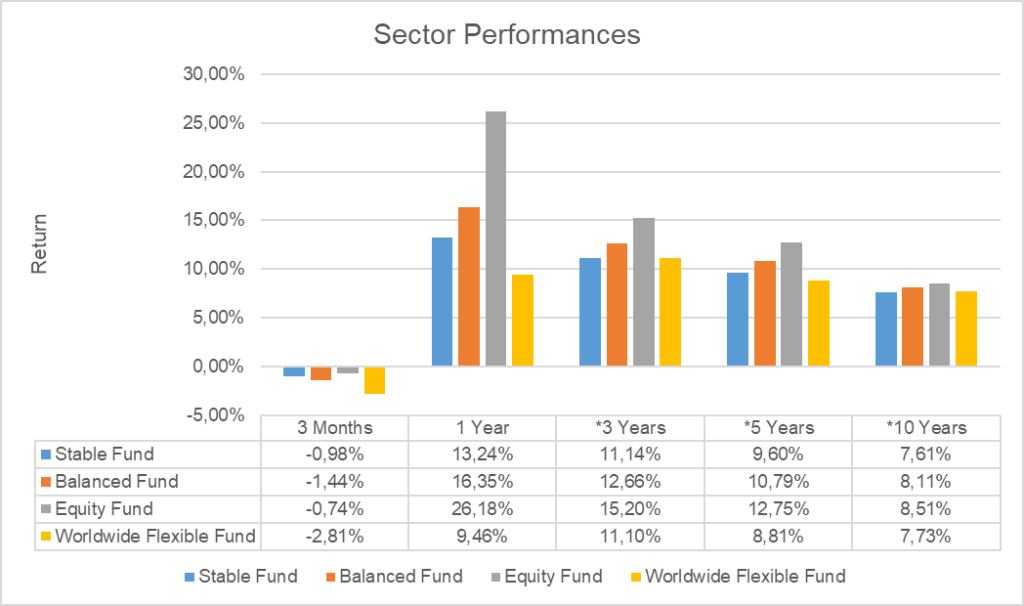

Source: Profile Data 31/03/2026

* Annualised Performance

Has the tide turned for South Africa?

It’s been almost 2 years since the national election that saw the ANC lose its majority, leading to the GNU. Since the formation of the GNU South Africa has seen various improvements despite the usual challenges.

Business confidence has increase over the last 2 years despite our poorly managed relationship with the US. Foreigners have been buying South African assets. 2025 saw foreign net holdings of South African bonds increase from 24.6% in 2024 to 25% in 2025. This number had previously been falling each year from 2017 – 2024.

Given the extreme bond and equity market rally in 2025 as well as a change in sentiment, has the tide turned for South Africa?

In November S&P Global upgraded South Africa’s national debt rating. Our first ratings upgrade since we were downgraded to junk status in 2020. In October the Financial Action Task Force (FATF) removed South Africa from the “grey list” after numerous actions were taken. No more cash under in the couch Mr president!

We have a lower budget shortfall (borrowing less), and our GDP(economic activity) is rising – albeit modestly so. Lastly, South Africa reduced its inflation target to 3% which is more or less in line with our emerging market peers. A decision that could lead to a lower depreciation in the rand over time.

Structural improvements have also been made to state owned enterprises such as Eskom and Transnet. Serious attention is also being given to the state of our ports which have been a structural headwind for growth. Private sector participation and infrastructure spending has also increased. An accumulation of small wins is certainly starting to add up for the country.

Economist Dawie Roodt has expressed a cautious optimism that the country may have reached a turning point. But he makes the point that this is not yet a certainty as challenges still remain.

Various well-respected economists gave their views on the recent national budget. Overall, the views were positive. Particularly given the environment that we have come from. Some of the concerns raised included the following:

- 20.6% of revenue goes towards debt servicing costs.

- GDP (economic activity) growth forecast is increasing year on year, but not enough to sustainably tackle the issue of mass unemployment, a consistent budget deficit and low levels of capital investment. Economist Dawie Roodt believes that GDP will come in lower than national treasury’s forecast over the next 2 years.

- The public sector wage bill is still out of control. Civil servants constitute 1.9% of South Africa’s population and yet 10.5% of the country’s GDP goes toward paying the public sector wage bill. What’s equally concerning is that the mid-term budget made an allocation for a 4.4% increase in the wage bill compared to an inflation target of 3%. Clearly government is not doing enough about curbing the wage bill.

- Personal and corporate taxes remain extremely high.

- South Africa’s GDP per capita in USD terms is well below the pre-covid high. Practically speaking, South Africans are on average getting poorer each year.

- National treasury calculations show that all social expenditure across the different functions of government accounts for about 60% of non-interest expenditure.

- High levels of corruption and cadre deployment continue to persist as evidenced by the Mhlanga Commission.

Despite having made real progress in just less than 2 years, South Africa needs to do more to ensure that the worst is behind us. Economist Dawie Roodt makes the point that we need to see high growth rates, higher than national treasury is forecasting, whilst Investec’s Chief Economist Annabel Bishop emphasises that government needs to contain its spending.

Economists agree that there has been structural progress in South Africa which is reflected in the higher business confidence numbers. There seems to be sentiment that South Africa has bottomed and that the outlook is far better than where we have come from. Nevertheless, we still have major issues such as high unemployment, an unsustainable social expenditure, high debt levels, mass corruption and infrastructure that’s in need of major capital investment. But none of this is new. It’s persisted for many years.

If South Africa can continue to accumulate small wins and emphasise policy decisions which continue to prioritise growth, its potential may surprise many a sceptic.

You don’t want too much fear in a market, because people will be blinded to some very good buying opportunities. You don’t want too much complacency because people will be blinded to some risk. Ron Chernow

The difficult balance is in recognising our biases which may blind us as investors.

Regardless of South Africa’s small wins and persistent challenges, local assets have continued to deliver attractive returns on the back of a constructive global environment.

FORWARD OUTLOOK (LOCAL)

Last quarter we discussed the expectation that volatility was to be expected and that the likes of Allan Gray and 36ONE were expecting to use volatility as an opportunity to buy growth assets at cheaper prices rather than a reason to structurally de-risk portfolios. In March the opportunity arose.

According to Alet Fick, senior multi-asset analyst at M&G Investments, “we made use of the opportunity presented to us during the market volatility to add assets to funds where we see compelling valuation signals. Within the SA equity market, we increased our asset allocation to move to overweight SA equities in most of our multi-asset funds during the March sell-off. Industrials (-8.4%) was the worst-performing sector in the SA market during the quarter, which provided the opportunity to increase our holdings in already cheap segments at even more favourable prices.”

Coronation, 36ONE and various other managers used the March sell off to increase their exposure to growth assets. Many of the asset managers hold an overweight position to growth assets which is a far cry from an environment where managers are concerned about a global recession and consequently hold a modest exposure to growth assets.

Thus far, the March sell off appears to have been a sporadic buying opportunity, much like the April 2025 Trump Tariff Tantrum moment that sparked global fears.

The International Monetary Fund recently announced a reduction to its 2026 global growth forecast assuming a short-lived Iran war. IMF Chief Economist Pierre-Olivier Gourinchas warned that the world is drifting toward an ‘adverse scenario’ of 2.5% growth in 2026. This compared to the previous estimate of 3.3% in January which has since been revised downwards to 3.1% and is a point of concern.

The bottom line is that this all comes down to the consequence of what’s happening in the Strait of Hormuz and the subsequent shock to energy prices.

If a swift resolution is reach, global growth fears are likely to subside. In an “adverse scenario” which isn’t a base case at this stage, South African economic growth numbers would surprise meaningfully on the downside. SA inflation would increase as a result of a higher fuel price and a weaker rand, and an increase in interest rates may be on the cards for 2026.

Not a great picture…

Fortunately, this is not the base case, and managers continue to hold overweight positions to very attractive growth assets.

In these scenarios it’s important to recognise that asset managers seldom take a binary view or one-sided view within the portfolios. They execute a rigorous risk adjusted return investment philosophy to cater for various outcomes, be it a more constructive growth scenario or a more adverse scenario. They constantly review their decisions and where necessary, changes are implemented on your behalf. A great example of this was the decision to use the volatility in March to increase growth asset exposure at attractive prices.

OFFSHORE MARKETS IN A NUTSHELL

Global equity markets struggled over the quarter as a result of the US/Iran conflict in March. The MSCI World Equity Index fell by -3.6% in US dollars. The broad US market fell -4.6% over the quarter. Emerging markets were relatively flat, down only -0.2%.

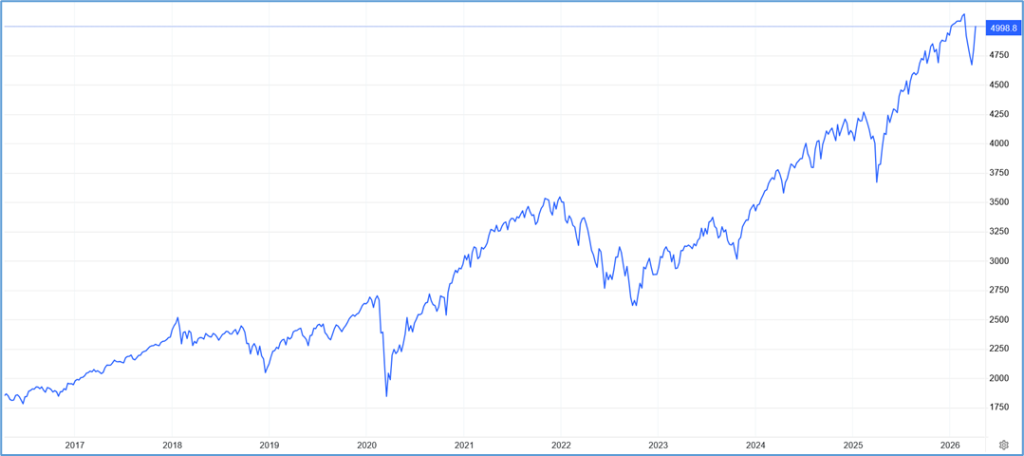

The graph below represents the global equity index over the last 10 years in US dollar terms.

Source: tradingeconomics.com

U.S. stocks declined, as a conflict with Iran and new tariff policies kicked off a five-week losing streak to close the quarter, erasing early-quarter gains. Rising oil prices gave a boost to energy stocks, while the materials and utilities sectors also performed well. The financials, consumer discretionary and information technology sectors each had near double-digit declines. Overall, the S&P 500 Index fell 4%, closing at its steepest quarterly decline since the first quarter of last year despite reaching several all-time highs earlier in the period.

The U.S. economy grew modestly, as gross domestic product (GDP) rose an annualized 0.7% in the fourth quarter, the slowest rate since a decline in the first quarter of 2025. Inflation was unchanged in February, with the Consumer Price Index (CPI) up 2.4% from the previous year, matching January’s figure. The unemployment rate inched up to 4.4%, ending two consecutive months of easing since November’s high of 4.6%

Emerging markets (EM) equities fell slightly during the quarter but outpaced many developed markets amid heightened volatility linked to the Middle East conflict. South Korea and Taiwan reported gains driven by robust demand for semiconductors and memory chips. Latin American equities surged following elevated foreign capital inflows. In contrast, Indian stocks declined on investor outflows while Chinese equities fell partly due to rising geopolitical uncertainty. Overall, the MSCI Emerging Markets Index fell 0.17%

Capital Group World Markets Review — First quarter 2026

What does the US/Iran war mean for my portfolio?

March has been a tumultuous month for the world, not only for energy prices but also for geopolitics.

Geopolitics is re-shaping the world at a rapid rate and herein lies the challenge for asset managers. How does one manage money in an environment of global structural changes? Investors are no doubt wondering what this all means for their investments both in the short and long term.

There are a few points to note about the changing world order and the exogenous shock factors that have become all too common.

April 2025 Trump Tariff Tantrum

Regardless of how one feels about Trump, he is a disruptor. Last year Trump placed tariffs on every major country in the world. This sent markets into a tailspin with global markets falling over 10% in USD terms in 2 days. Within a week Trump announced a 90 day pause on the tariffs stating that markets were getting “a little bit yippy”. Within a month markets had fully recovered from the knee jerk reaction.

Despite Trump’s aggressive “America First” rhetoric, the idea of ultimate American dominance over the world came with the caveat that the US needs the rest of the world to be in a functional economic state. Lest one forgets that the US economy is the biggest in the world by some margin. It does not exist in isolation from the rest of the world.

March 2026 US/Iran War

In March the US and Israel led a bombing campaign against Iran. The main reason for Operation Epic Fury was to neutralise Iran’s ability to develop nuclear weapons and to destroy its hierarchical dictatorship. Less than 2 weeks into the war Trump stated that the war will be over “soon” with them “pretty much at the end of the line”. The war has extended beyond what was initially expected with Iran successfully closing the Strait of Hormuz leading to a worldwide oil shock and spike in energy prices.

According to Capital Group Economist Jared Farnz, “in the U.S., oil at $120 a barrel would be enough to cut GDP growth by 1.5 percentage points to around 1% or less,” Franz adds. “This would also likely lead to a global energy-induced recession.”

Recently on a Truth Social post, Trump stated that “a whole civilization will die tonight, never to be brought back again. I don’t want that to happen, but it probably will”. Hours later Trump announced a two-week ceasefire with Iran. Markets immediately started to rally on the news. At the time of writing, equity markets are around 2% – 2.5% away from their all-time highs. Having almost entirely recovered from the events in March.

It’s clear that the US has overplayed its hand. However, Trump is not one to back down. As the ceasefire talk progresses, both sides will be looking for a solution as a drawn-out war won’t benefit either side. The world waits in hope that a deal is reached.

Trump’s actions and comments towards its closest allies in Europe have left the world in a vulnerable place. It wasn’t all that long ago that Trump threatened to acquire Greenland. Trump indicated the U.S. might take the territory regardless of whether Denmark “likes it or not”.

As diplomatic relations have broken down, France has repatriated all of its gold reserves that were being stored in the US, which political analysts believe could spark a trend amongst other European countries.

EU officials stress that various measures have been taken towards “de-risking” Europe’s relationship with the U.S. by looking towards being less reliant on them, rather than completely “decoupling”. German Chancellor Friedrich Merz recently stated “If we want to be taken seriously again, we will have to learn the language of power politics”.

President of the European Commission Ursula von der Leyen called on the EU to strengthen its “economic power”, diversify its supply chains and become more independent vis-a-vis the US.

The writing is on the wall. Europe must become less dependent on the US if it is to be an equal partner.

But what does that mean for you and your portfolio?

In many ways Trump issued in a new era of populist politics of which the underlying narrative is anti-establishment through radical change.

It’s this radical change that the world is at odds with. But much like Trump’s first presidency, countries and economies eventually adapt to the prevailing environment.

Trump’s second term was never going to be smooth sailing.

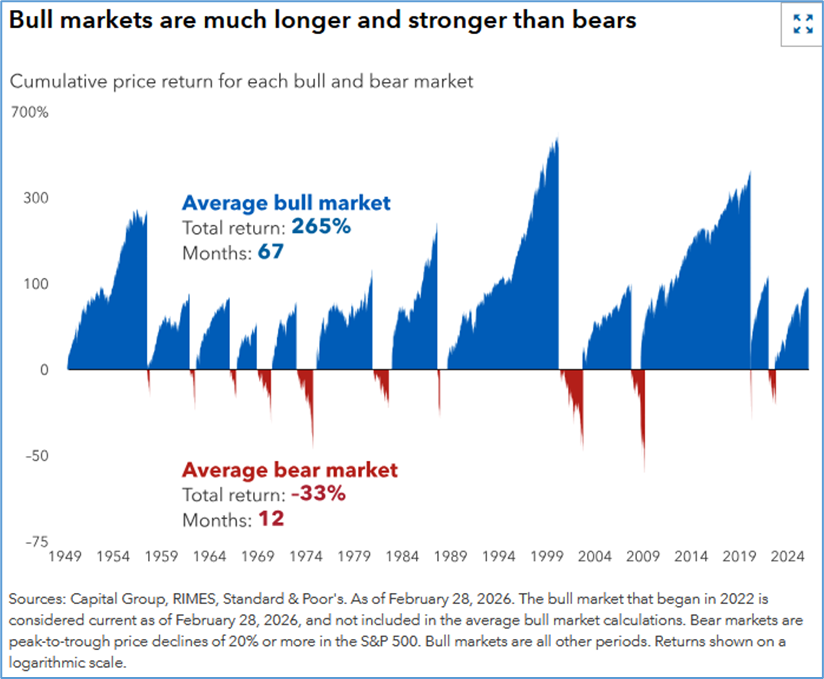

The chart below uses the S&P 500 to illustrate periods of bull markets (markets going up) and bear markets (markets going down by at least 20% or more). The chart makes the point that bull markets last meaningfully longer than bear markets with the average bull market lasting around 67 months with an average return of 265%. And yet, investors tend to panic during bear markets. Some even try to time the entry and exit of the market based on the emotional states of fear and greed.

Of the 11 bear markets shown in red, only four of them occurred outside of a recession. Namely 2022, 1987, 1966, 1961-1962. The average time that it took the market to fall to its lowest point during those periods was just over 6 months. If you compare this to periods where the world fell into recession, it typically took between 14 and 18 months for markets to bottom and start their recovery. A much longer period.

It’s therefore important to recognise whether a bear market or indeed periods of heightened volatility is as a result of geopolitical shifts and exogenous shock factors, or whether it’s related to a looming global recession.

Had an investor sold some or part of their investments, after the Trump Tariff Tantrum in April 2025 or indeed the March 2026 US/Iran war, investors would have destroyed capital as the fall in the market was short lived despite the anxiety around the events.

For investors, it’s important to remain committed to their financial plans. Decisions should not be made in response to fear.

FORWARD OUTLOOK (OFFSHORE)

All eyes are on Trump and the outcome in the Middle East. Both the US and the rest of the world need a lower oil price. If the status quo was to continue, it could have an adverse effect on global inflation and as a consequence, global growth.

Given the upcoming mid-term elections in the US and deteriorating diplomatic relations between the US and its major allies, Trump needs a resolution to the Iranian issue.

Another concern which could be around the corner is a possible tariff 2.0. In February a US Supreme Court ruled that tariffs imposed by President Trump under the International Emergency Economic Powers Act (IEEPA) were illegal. Trump has since suggested that a new round of tariffs is being considered under different legislation. Given the deteriorating political ties with its allies in Europe, one wonders how this would all play out.

Regardless of any tariff decisions made by Trump in the coming months we urge investors not to make any decisions based on the news, should it occur, or any subsequent volatility that may follow. Much like April 2025, the world adapts to the environment and so do the fund managers.

The larger economic concern is around global inflation.

Disclaimer: The value of investments can go down as well as up. Investors may not get back the value of their original investment. Past performance cannot be relied on as a guide to the future. Changes in exchange rates may have an adverse effect on the value, price or income of foreign currency denominated securities. Investments and other services available through Asset Protection International may not be suitable for all investors. Asset Protection International does not make any warranty, expressed or implied, about the accuracy, completeness, or usefulness of any information disclosed herein. Any reliance upon any information in this document is at your sole risk. Asset Protection International and its financial advisers will not be liable to anyone for any direct, indirect, special, or other consequential damages for any use of information obtained in this document.