2026 FIRST QUARTER COMMENTARY

LOCAL MARKETS IN A NUTSHELL

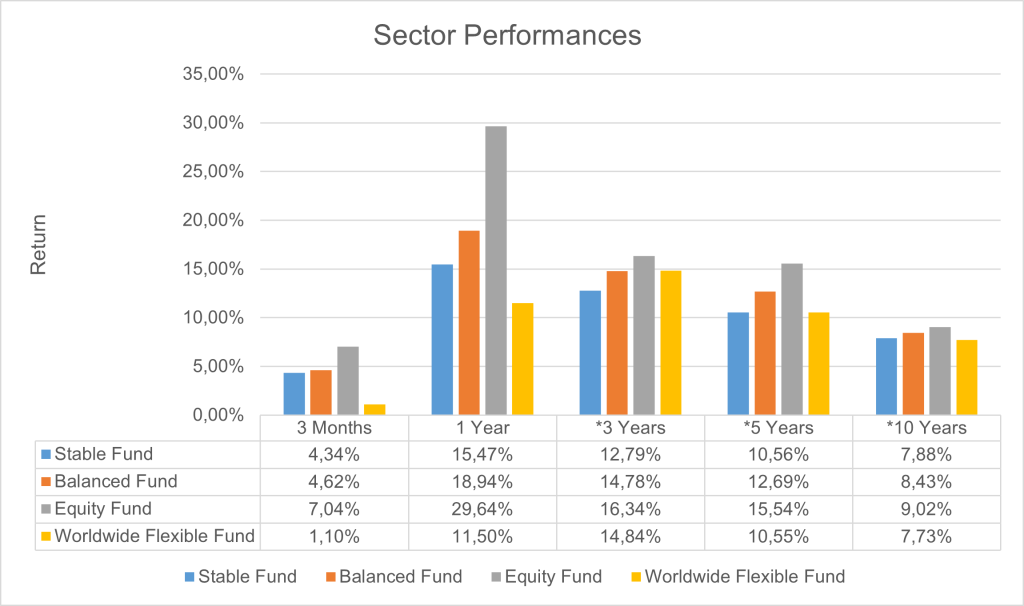

Over the quarter the FTSE/JSE All Share Total Return Index gained 8.1%. Financials gained 17.6% whilst the resource sector continued to shine, up 8%. Industrials were slightly negative over the quarter at -0.5%. South African Mid and Small Cap stocks (a proxy for South African-centric stocks) rose 8.7% for the quarter.

South African bonds returned a staggering 9% for the quarter.

Chart: Performance of the FTSE/JSE All Share Index over the past ten years (2016/01/01 – 2025/12/31)

Source: tradingeconomics.com

The FTSE/JSE All Share Total Return Index delivered 42% in 2025, the highest calendar year return from the local stock market since 2005. The majority of the return was attributed to precious metal miners such as gold and platinum mining stocks along with technology giants Naspers and Prosus.

The FTSE JSE All Bond Index delivered a return of 24% for the year. It was the best calendar return from the local bond market since the turn of the century.

Interest rates were cut by another 0.25% in November. Interest rates have fallen by 1.5% since September 2024 with many arguing that the South African Reserve Bank has further room to cut as a result of our low inflation rate.

Overall consumer confidence ended the year higher whilst business confidence remained relatively flat albeit above the average for the last 3, 5 and 10 year period.

Over the quarter the rand strengthened by 4% against the US dollar and 3.7% versus the UK pound. Over the course of the year the rand strengthened by 12.2% against the US dollar and 5.2% against the UK pound.

How do top managers view the local markets going into 2026?

After posting its best calendar year return since 2005, does the local stock market still offer opportunity or is the horse all but spent? One could ask the same question of the local bond market which delivered its best calendar return since the turn of the century in an environment where inflation was relatively low.

We asked two top managers to comment on their 2026 outlook and how their funds are positioned.

Both Allan Gray and 36ONE hold overweight positions in local equities compared to peers. Both managers sighting the same overarching themes which includes lower inflation, lower interest rates, the potential for continued strength in precious metals, as well as a more supportive backdrop for local businesses. Other factors include a potentially weaker USD.

The expectation for economic growth or GDP growth in 2026 is meaningfully higher than 2025. SA GDP is expected to come in at around 1.2% according to the International Monetary Fund (IMF) for 2025 whilst Investec Chief Economist Annabel Bishop expects GDP growth of around 1.5% – 1.6% in 2026. Although we are moving in the right direction, is GDP growth of 1.5% enough to improve South Africa’s fiscal or economic woes?

Econometrix Chief Economist Dr Azar Jammine, was recently quoted saying “I think saying South Africa’s economy is out of the woods is an overly strong statement. There are still huge challenges to be confronted. All that we can say at this time is that there are signs that maybe we have seen the worst and that things are starting to improve gradually. The emphasis is on ‘gradually’.”

This highlights the ongoing concerns that Allan Gray, 36ONE and many top managers have around SA and the local markets.

Politics undoubtedly remains the biggest risk to South Africa. According to 36ONE local political developments will likely create uncertainty. “We would view municipal election-related dislocations as potential buying opportunities rather than reasons to structurally de-risk. As South Africa evolves toward more coalition-led governance, market focus is shifting toward the pace and credibility of municipal reform. This is a multi-year process, with groundwork already underway through initiatives such as Operation Vulindlela.”

Allan Gray highlights that the outlook for locally focused (“SA Inc”) shares could worsen if the Government of National Unity’s (GNU) working relationship deteriorates, structural reform plans stall and/or economic growth remains lacklustre. Continued fiscal strain, marked by rising government debt-to-GDP and interest costs consuming an increasing share of tax revenue, would further weigh on investor confidence.

Despite the outlook for improved economic growth in 2026, South Africa’s debt to GDP is expected to continue to deteriorate. It is believed that South Africa requires annual GDP growth closer to 2.5% – 3% to meaningfully alter the long-term trajectory.

Despite this expectation, continued improvements in South Africa suggest the potential for positive returns going forward.

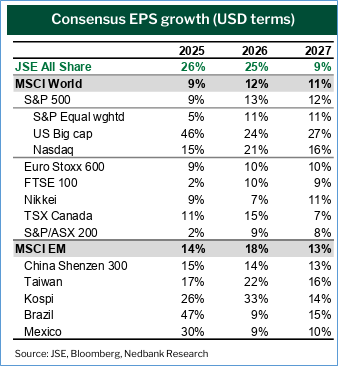

The table below shows the consensus earnings per share growth in USD terms for the local stock market (shown in green) compared to various other equity markets. What’s noticeable is the 2026 earnings per share growth of 25% with a further 9% expected in 2027.

Note that this is not a prediction of returns, but rather an emphasis on the direction of earnings growth which is a fundamental driver to long-term returns.

Allan Gray makes the point that “given the very strong performance of the All Share Index in 2025 (largely driven by Naspers/Prosus and record precious metal prices), we would not be surprised to see some consolidation in 2026 and continue to tilt the portfolio towards defensive rand hedges. At the same time, we continue to find opportunities among SA Inc shares where valuations have become increasingly attractive, with many having sold off from their post-election highs.”

This corelates to 36ONE’s view that volatility is to be expected for various reasons, however they note that volatility would be used as potential buying opportunities rather than reasons to structurally de-risk. In other words, they expect to use volatility as an opportunity to buy into companies rather than as a signal that the proverbial wheels are falling off the cart.

OUTLOOK (LOCAL)

The outlook for 2026 is positive with managers such as Allan Gray, 36ONE and Coronation holding overweight positions to local equities. Earnings growth is expected to continue to deliver very attractive returns.

Geopolitical risk is as ever front of mind, however, volatility is viewed as a buying opportunity. The likes of Allan Gray have tilted the portfolios towards defensive stocks as they believe that some consolidation (volatility) could be expected over the course of the year. Others such as 36ONE have acknowledged that bouts of volatility are inevitable over the over the course of the year and that such events would be used as a buying opportunity rather than a reasons to structurally de-risk portfolios.

We therefore encourage investors to share a similar mindset. In the absence of any fundamental changes in their financial plan, periods of volatility should not be viewed as reason to de-risk their portfolio but to rather remain committed to their unique financial plan.

OFFSHORE MARKETS IN A NUTSHELL

Global equity markets continued to deliver strong returns over the quarter. The MSCI world equity index gained 3.1% in US dollars. The broad US market rallied 2.3% over the quarter. Emerging markets were up 4.7%.

The graph below represents the global equity index over the last 10 years in US dollar terms.

The global economy showed signs of gradual softening in both growth and inflation. The IMF’s October 2025 World Economic Outlook projects global GDP growth to decelerate from 3.3% in 2024 to 3.2% in 2025 and further to 3.1% in 2026. Headline global inflation is expected to ease from 4.2% in 2025 to 3.7% in 2026, as supply constraints diminish. Inflation abated in the US, UK and Eurozone for November supporting the ongoing easing cycle, even as longer term yields climbed amid fiscal sustainability concerns.

The US central bank continued lowering interest rates in the fourth quarter, further driving an easing of financial conditions. US interest rates have fallen by 1.75% since September 2024 with further rate cuts expected in the first half of the year.

On the 1st of October the US government “shutdown” as policy makers were unable to find a consensus on a proposed government funding bill. What followed was the longest US government shutdown at 43 days. It was somewhat surprising that the market largely overlooked the event. What it highlights is the continued rampant spending by the US government.

A year ago, the Department of Government Efficiency (DOGE), was established to cut wasteful expenditure, to which it was largely successful having saved an estimated $215B to date. Various estimates believe that the additional tariff revenue will comfortably exceed this number.

It remains to be seen whether the US will be able to continue to manage its debt to GDP leaving room for continued political turmoil in the US mid-term election year.

Commodities remained a centrepiece for market performance, with precious metals notably strong. Gold extended its advance, surpassing record levels amid heightened geopolitical tensions and expectations of further US rate cuts in 2026.

A rapidly changing world and the implications for 2026

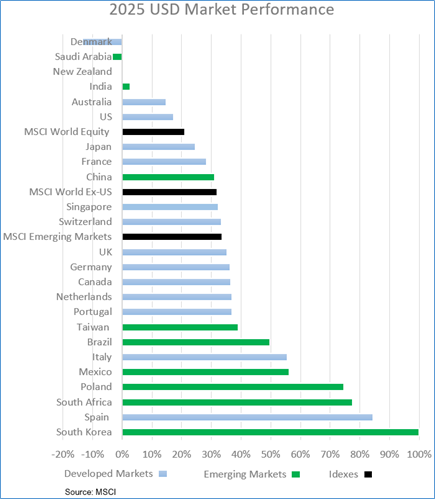

2025 was a great year for returns in most equity markets. The US market delivered over 17% for the year. The more surprising outcome was the degree to which the US underperformed both the average developed and emerging market. The chart below shows the 2025 USD returns from various developed and emerging markets as well as select equity indices.

For years, the US market has been viewed as relatively expensive with many touting the attractiveness of markets outside of the US. 2025 was a year where many underpriced markets rebounded relative to the US. Even on a 3 year basis the MSCI World ex-US (excluding the US), a predominantly developed market global equity index, has delivered an annualised return of 17.6% compared to the US with 22.7%

If one were to have compared the 3 year annualised performance as of the end of 2024. The MSCI World ex-US would have delivered a return of 1.9% compared to the US at 8.1%.

These numbers serve as a glaring reminder of how quickly trends can change.

Some of the more common concerns that investors are expressing include the following:

- Could this be the start of the end of US exceptionalism (US dominance)?

- Is the US in an AI bubble?

- Could geopolitical tensions de-rail the global economy?

Trying to form a reasonable expectation based on a variety of informed views has become increasingly difficult.

Allan Gray believes that opportunities remain compelling outside the US where valuations appear more reasonable and fundamentals are improving. They are particularly constructive on emerging markets as are many other global managers such as Coronation, Ninety One, Foord, Dodge & Cox and FPA.

One of Allan Gray’s concerns regarding the global equity outlook is the potential for US mega-cap technology stocks (very large US tech companies) to outperform, extending their dominance and driving global index returns.

In other words, they are concerned that a large, expensive part of the market could continue to become more expensive leading to potential bubble-like dislocations between actual fundamentals and unwittingly poor investor perceptions. Last year’s underperformance by the US market relative to the rest of the world was a healthy correction in what had become an ever-increasing dichotomy between actual fundamentals and investor expectations.

One of the other concerns flagged by Allan Gray is the rising protectionism and escalating geopolitical tensions that could weigh on sentiment particularly in emerging markets despite attractive valuations.

In layman’s terms, despite the fact that emerging markets are attractively priced with improving fundamentals (viewed as a great environment for investment opportunities) geopolitical tensions can cause asset prices to remain low or dislocated from fundamentals for extended periods of time.

36ONE is of the view that global economic growth will be resilient alongside lower US interest rates, which together typically creates a supportive backdrop for growth assets.

Importantly, they feel that the global consumer will remain resilient and a key support for the global economy.

Some of the key risks that they have highlighted are elevated US valuations (an expensive stock market), pockets of which are at risk of correction (a fall in value) and as such, they have maintained some protection in their hedge funds. They are also concerned about the potential for a sharper than expected slowdown in global growth as well as a re-acceleration in inflation that delays or limits interest rate cuts in the US.

Simply put, these two managers, along with many of their peers, are still optimistic about the potential for attractive returns. Many of the “risks” that they highlight, are well known – geopolitical tension, a potential resurgence in inflation, high US valuations etc to which they are closely monitoring.

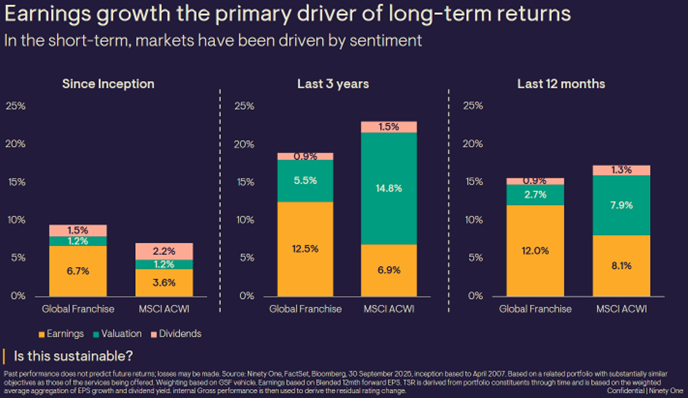

In an October interview, Ninety One portfolio manager Clyde Roussow shared an update where he touches on the reason why the S&P 500 and the general US market has delivered most of its return over the last few years from what we call “re-rating” ( where the share price has simply gone up based a change in sentiment) rather than earnings growth (which should be the main long-term component of one’s return). In other words, the price should follow the earnings and not the other way around.

The chart below shows the return components of the Ninety One Global Franchise Fund which is run by Clyde and his team, compared to the MSCI All Country World Index.

The orange box should make up the majority of the return component (earnings). Over the last 3 and 5 years, the green box (re-rating or change in price) has made up the majority of the return.

This has to either moderate (become less spectacular) or revert back to the mean (perhaps de-rate) at some point.

Up until now it’s just been a very easy, seemingly one way move for the US market and tech in particular. It’s perhaps a dangerous assumption to believe that this will continue at this point in the cycle.

What the chart also shows is that the fund’s return has been primarily driven through earnings growth rather than re-ratings. The earnings growth of the companies that the fund holds is meaningfully higher than that of the market. This should give investors a great deal of comfort despite the fact that the fund’s recent performance is behind that of the index.

This illustrates Allan Gray and 36ONE’s views that there is fundamental opportunity within global markets. This refers to good businesses with growing earnings streams that one can buy at an attractive price.

FORWARD OUTLOOK (OFFSHORE)

In the absence of exogenous risk factors, one could argue that that select global markets look attractive with top fund managers holding an overweight position in global growth assets relative to peers.

High relative valuations in the US continue to be an area of concern for most managers. There is a question around whether a major sell off in large expensive US equities could cause a sell off in global markets. This remains to be seen. However, managers are prepared to use bouts of volatility to purchase growth assets at lower prices. One should therefore be of the view that should a sell off occur, the various managers within one’s portfolio will actively navigate the environment without the need for intervention from investors.

Disclaimer: The value of investments can go down as well as up. Investors may not get back the value of their original investment. Past performance cannot be relied on as a guide to the future. Changes in exchange rates may have an adverse effect on the value, price or income of foreign currency denominated securities. Investments and other services available through Asset Protection International may not be suitable for all investors. Asset Protection International does not make any warranty, expressed or implied, about the accuracy, completeness, or usefulness of any information disclosed herein. Any reliance upon any information in this document is at your sole risk. Asset Protection International and its financial advisers will not be liable to anyone for any direct, indirect, special, or other consequential damages for any use of information obtained in this document.