The Gold Conundrum

Gold has become one of the hot topics in 2025 with its year-to-date price surge of around 60% in USD terms.

Common questions that we are receiving from clients include the following:

- Is it a good time to buy gold?

- How much gold do we have in the portfolio?

- Does this mean that we are headed for a global recession?

- Is this because of the unsustainable levels of debt around the world?

Clearly the rally in the gold price is raising more questions than answers and in such an event, one should step back and consider the evidence in an objective manner.

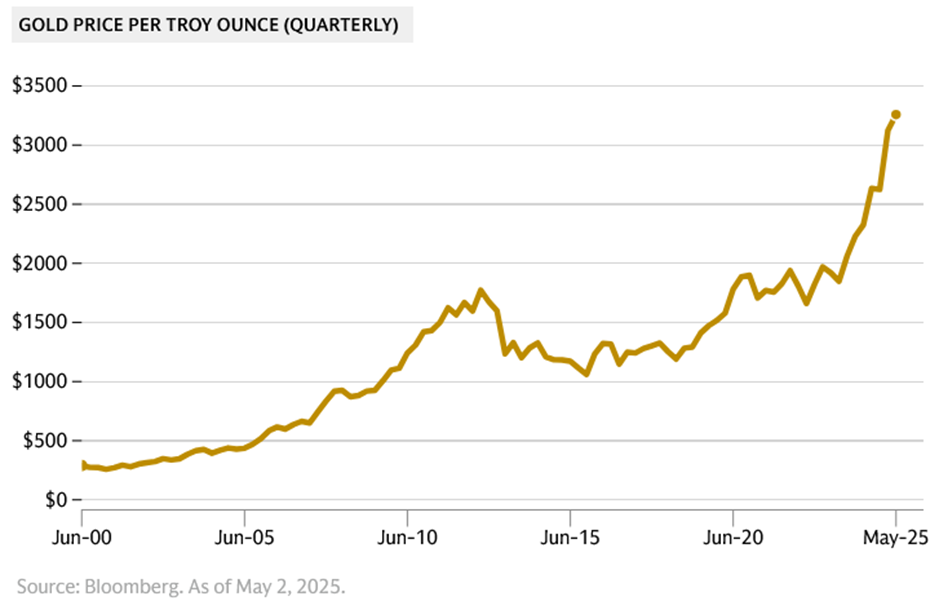

The chart below shows the gold price in US$ / Oz since the year 2000.

A logical question to ask is what’s driving the parabolic price increase over recent years.

Gold as a strategic reserve

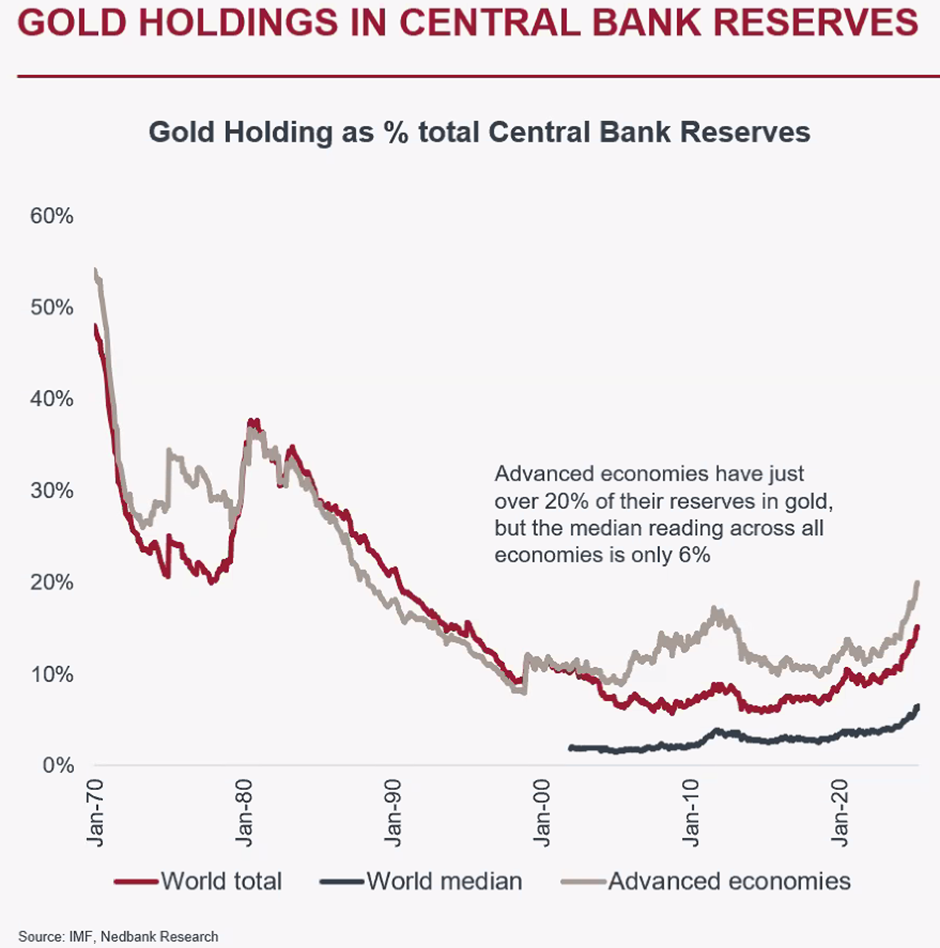

The chart below shows that since the US went off the “gold standard” in 1971, a period where every US$ was backed by gold reserves, gold held by central banks has declined as a percentage of total central bank reserves. In recent years, central banks have been buying gold to shore up these reserves.

Most notably, advanced countries such as the US, Germany, France, Italy, Portugal, Netherlands and Austria hold over 60% of their total reserve holdings in gold. On average advanced economies hold 20% of their total reserve holdings in gold. This is a far cry from the 6% average across all economies. Highlighting the modest exposure held by emerging economies.

Emerging market central banks, which have a smaller percentage of their reserves in gold, are also playing catch up with their peers in developed markets. According to Goldman Sachs Research, China holds less than 10% of its reserves in gold, compared to about 70% or more for the US, Germany, France, and Italy.

Developed economies’ large gold holdings are partly a legacy of the gold standard era, when sovereign money supplies were linked to gold

Traditionally, emerging market countries such as China, Russia, India, Brazil etc. have held US Treasuries (US debt) as a reserve asset.

Prior to Russia’s invasion of Ukraine, it systematically reduced its exposure to US Treasuries in favour of gold. In hindsight, this was clearly a deliberate strategic move by the Russians.

What traditionally helps to drives the price of gold?

Gold is seen as both a store of value and a safe haven asset. During times of high inflation or geopolitical uncertainty, gold has historically done relatively well.

Gold like other assets, is also subject to economic cycles. In other words, there are macro-economic factors that help to drive the price of gold.

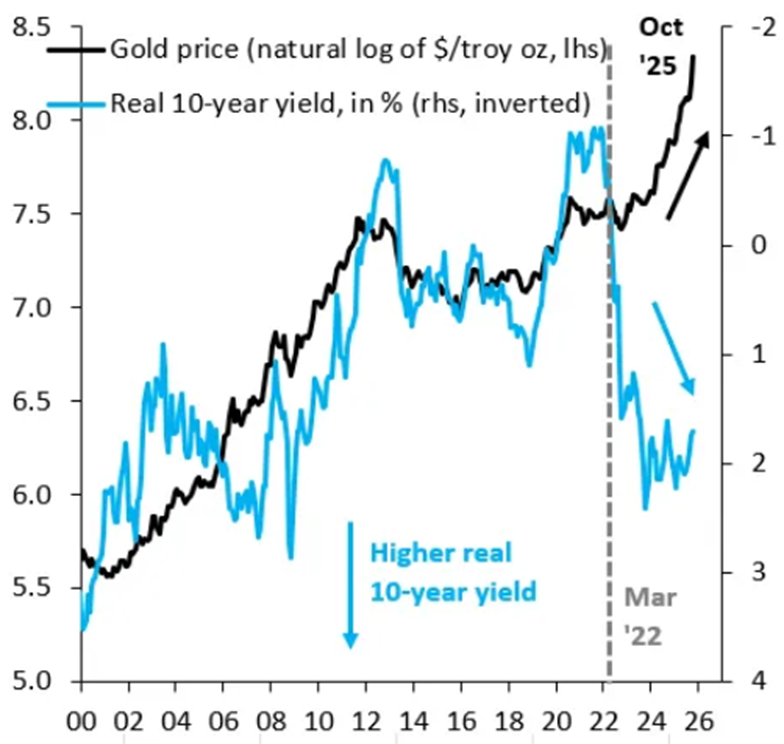

One of these factors is related to US Treasuries (US debt market or bond market). As per the chart below, when US Treasuries offer a low return relative to the rate of inflation, gold tends to do well. This is simply because countries, institutions, asset managers, investors, tend to buy gold as a store of value and as a safe haven asset rather than buying US Treasuries that offer a yield that is similar to the rate of inflation.

What’s evident in the chart below is that in March 2022, this trend completely broke down.

Source: Goldman Sachs Global Investment Research, Robin J Brooks

What’s driving the current rally in gold?

In March 2022 the US froze Russian assets invested in the US including US Treasuries in response to the invasion of Ukraine.

This sent a very dangerous message to the world. If given the will, the US can freeze foreign assets at their discretion.

Remember the context of emerging economies holding significant exposure to US Treasuries relative to gold reserves.

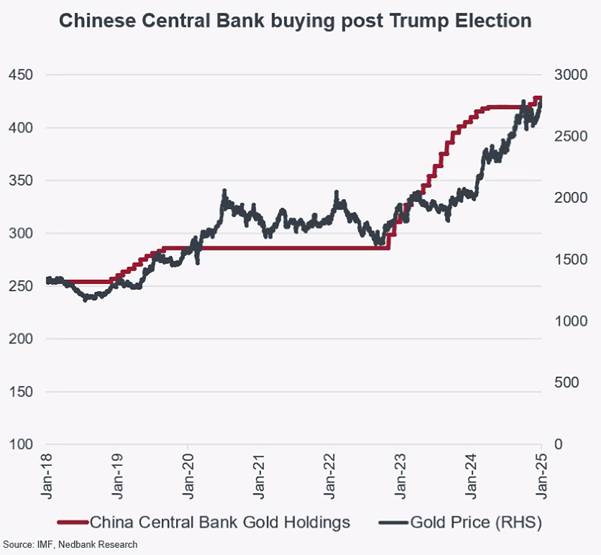

For a country such as China where there is often geopolitical tension, a strategic shift out of US Treasuries in favour of gold is of paramount importance.

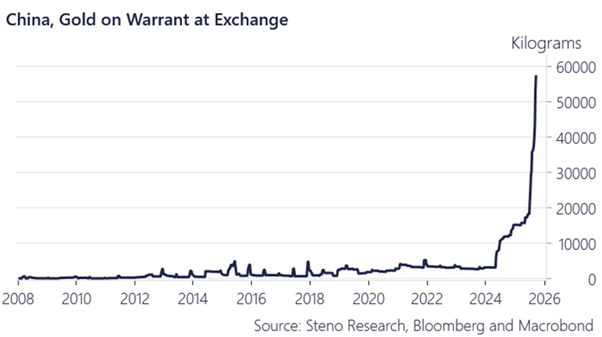

As the chart below shows, China has been an aggressive purchaser of gold.

The chart below shows the extent to which China has been buying gold relative to its historical average.

But China isn’t the only central bank to buy gold. Central banks around the world have been net buyers of gold.

This surge in central banks gold purchases also reflects a broader global transition — from West to East. While Western economies still rely heavily on the dollar-based system, the BRICS nations (Brazil, Russia, India, China, South Africa — soon joined by others) are exploring alternatives.

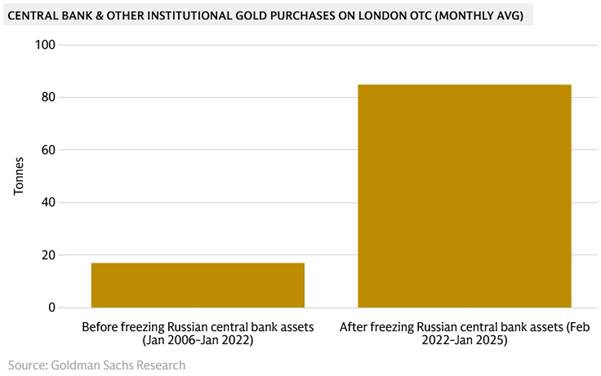

The chart below highlights the contrast between the purchase of gold pre and post the freezing of Russian assets.

The move by the US to freeze Russian assets was clearly a turning point in the status quo.

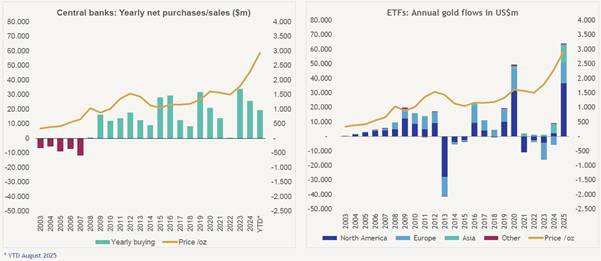

It’s not just central banks that are driving up the gold price.

The chart on the left shows that central banks are still net buyers of gold. However, the rate of purchases is slowing as the price of gold has increased. The chart on the right shows that gold ETF’s (exchange traded funds) have been extreme purchasers of gold in 2025 up to the end of August. This is largely driven by institutional and retail purchases of gold.

Source: Coronation

Why have institutional and retail purchases of gold been so high of late. Allan Gray portfolio manager Talia Petousis suggests that it’s been partly due to the fact that the world has become so indebted leading to fears around sustainability.

Is it a good time to buy gold?

We certainly don’t have the answer. The opinion around the gold price has become a contentious one after its recent surge and in light of changing supply and demand dynamics.

Conventional wisdom may suggest caution after gold returned in excess of 100% in USD terms over the last 2 years.

Structurally, the gold market may have changed as countries seek to shore up their gold reserves having seen the vulnerabilities in holding US assets – particularly for those who do not align with western interests and given their ballooning debt levels. Having said that, of late central banks have reduced the rate at which they have been buying gold. Will it reaccelerate? That remains to be seen.

Is China’s meteoric buying frenzy likely to continue at the current rate? One must acknowledge that it is possible if they wish to drastically change the composition of their reserve assets.

Allan Gray portfolio manager Talia Petousis suggests that if China wants to materially alter the mix of their reserve assets in favour of gold, they would have to continue buying a significant quantity of gold which may lead to a lack of supply in the market. In other words, there may not be enough gold in the market to meet the demand. This would be very positive for the gold price. Is this structurally where we are headed?

36ONE’s portfolio manager Matthew Whitelaw suggests that we would need to see a step up in global inflation to justify the current parabolic price movement in gold. Suggesting a more sober outlook for the commodity from current levels.

Coronation who holds an exposure to gold, share their views in their latest commentary:

“We note a significant investment conundrum for both gold and gold equities. Both the gold price and South African (SA) gold miners are trading at all-time highs, and commentary and news headlines suggest we are in the “frothy phase” of a bull market.

“The bull case for gold rests primarily on increasing systemic risks and consistent, price-insensitive central bank buying. This buying activity is a reaction to the US weaponisation of the dollar, following Russia’s invasion of Ukraine, coupled with fears that future administrations might further undermine the dollar or attack the independence of the Federal Reserve. Other major drivers include increasing global geopolitical risk, such as brittle US-China relations, and the slow-brewing crisis associated with overindebted sovereigns globally. Given these accumulating risks, gold is seen as one of the very few legitimate monetary assets and hedges, which remains under-owned by global investors looking for an alternative to fiat currency.

“Despite the compelling bullish arguments, we maintain a cautious stance. Historically, every comparable gold bull market has been followed by a downcycle, resulting in steep losses for shareholders. Costs tend to follow prices higher, albeit with a lag. We expect the same from this cycle.”

As one can see, the argument around gold both structurally and strategically is extremely complex. Convincing arguments can be made both for and against a further gain in the gold price.

Given the uncertainty around the future for the gold price, many asset managers have elected to hold an exposure to either gold and or gold miners with some being meaningfully underweight and some that are meaningfully overweight. Reflecting the uncertainty.

For further information and views on gold we recommend that you listen to a recent Allan Gray podcast on Gold in the age of fiscal dominance.